India’s Balancing Act

Portfolio manager Peeyush Mittal and research analyst Swagato Ghosh say India has a fiscal playbook to chart a path of stability and growth.

India, the equity market, has captured a large share of wallet and mind among emerging-market investors in recent years thanks to outperformance versus peers and optimism over its long-term prospects and potential. While secular trends and high-performing companies have dominated headlines, relatively little ink has been used to discuss the back-end engine powering India’s growth—its US$3.3 trillion economy, and how the government has managed the dual tasks of balancing the books and driving structural reforms.

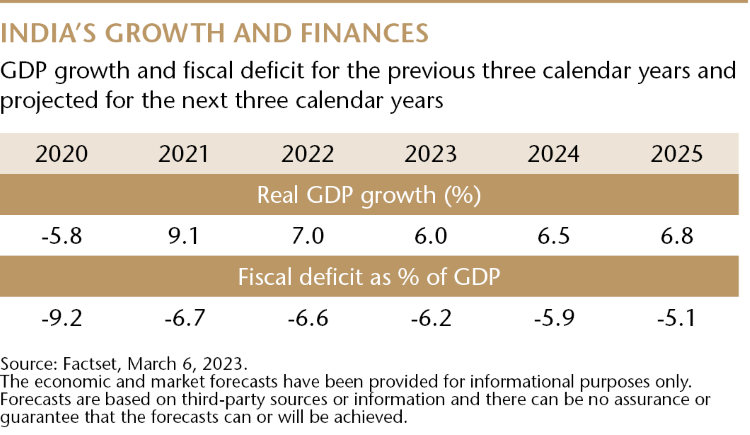

India’s fiscal state of health came into focus in February’s budget, the country’s last major financial statement before the general elections next year. The government projected a budget deficit for the financial year (FY) ending April 2024 of 5.9%, down from 6.4% projected for FY23, and a nominal gross domestic product (GDP) growth target of 10.5% versus 16% for this financial year. In terms of growth drivers, infrastructure spending will remain a key lever. The government ramped up its capital investment (capex) target by 33% to $122 billion for FY24. That’s three times the level of FY20 and will account for 3.3% of GDP next year.

In a growth-starved and heavily leveraged world, India’s balance sheet and growth outlook seem exceptional to us. Fiscal deficit projections are supported by tax revenue growth assumptions which are reasonable in our view and the resultant borrowing is already priced into government bond yields. Meanwhile, India’s capex stance should have a multiplier effect. It should not only directly create jobs and economic activity but there’s a good chance the resulting infrastructure expansion across sectors including transportation, health care, energy and defense, will have a knock-on effect leading to higher productivity and growth in other economic segments.

“In a growth-starved and heavily leveraged world, India’s balance sheet and growth outlook seem exceptional.”

It’s not all a bed of roses. Like many other economies, inflation is biting in India and domestic consumer demand weakened notably in the third quarter of FY23. Critics argue that the Modi government should be doing more to boost consumption and incentivize business but it’s not clear the government will heed the call. Even during the pandemic years, the government didn’t intervene too much on the demand side—focusing more on supply supports and tools for increasing capacity and production. The budget was a continuation of that strategy.

India’s government, we believe, should get credit for keeping control of the purse strings especially in a pre-election year. It has done a good job of not extending direct welfare benefits outside of maintaining the free food program for the very poor. This austerity is what has helped the regime keep its fiscal deficit target at an impressive below-6% level. That said, the lack of material incentives on the personal income tax side in the budget was disappointing. Measures for encouraging private capex would also have been timely.

In conclusion, last month’s budget was a balanced and pragmatic one, devoid of too many surprises and shocks. It added to the global perception that India has the ability to be financially prudent and at the same time produce robust growth. But it’s not a time to celebrate. A slowdown in consumption is visible and India’s current account deficit—imports versus exports—remains at an uncomfortable level. The fiscal year ahead will be tough. The government needs to stay true to its course and not deviate in its pre-election spending. A moderation in macroeconomic and external headwinds would also be welcome. We think if India successfully navigates these waters it has the opportunity to cement its standing as one of the most consistently growing major economic powers in the world.

Peeyush Mittal

Portfolio Manager

Matthews Asia

Swagato Ghosh

Research Analyst

Matthews Asia

Definitions:

Nominal gross domestic product (GDP) includes real GDP and inflation; real GDP is an inflation-adjusted measure that reflects the value of all goods and services produced by an economy in a given year.