Outperformance in Extraordinary Times

How the Matthews Emerging Markets Equity Fund’s strategy helped it achieve outperformance during a historic period for global markets.

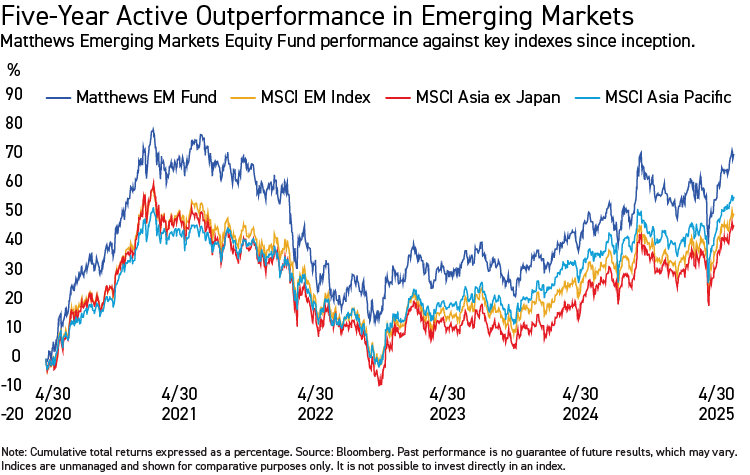

The Matthews Emerging Markets Equity Fund, the core growth portfolio in our suite of emerging markets products, celebrated its five-year track record on April 30. It was launched in 2020 at a time when COVID-related lockdowns were on the rise and China—a key country market in the emerging markets asset class—would shortly enter a downturn from which it has only started to recover from in the past 12 months.

Despite the challenging times, the Fund outperformed its benchmark, the MSCI Emerging Markets Index, by 2.43% and delivered a 9.21% annualized return over five years (as of April 30, 2025). This was against a backdrop of a weakening Chinese equity market and a U.S. market supported by American exceptionalism and “Magnificent Seven” big tech stocks.

We attribute this outperformance to our wholly active approach, a component absent from passive-based index-tracking mandates. The Fund’s strategy is designed to manage a well-balanced portfolio that can navigate different and evolving market conditions. It requires flexibility, aiming to participate in up markets, preserve capital during times of market stress and compound performance to generate compelling risk-adjusted returns.

Back in April of 2020, volatility was starting to enter the markets as lockdowns increased and the magnitude of the COVID crisis was becoming clearer. Russia’s invasion of Ukraine in February 2022 further heightened uncertainty. At the country level, China struggled through much of the period while other markets, like India, began to do very well.

We had to work hard at adjusting our exposures and calibrating our positions to protect our returns over the period. It was an intense time for markets but our investment approach effectively navigated the challenges by managing risk and return at both the country and company levels.

All performance quoted is past performance and is no guarantee of future results. Investment return and principal value will fluctuate with changing market conditions so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the return figures quoted. Returns would have been lower if certain of the Fund's fees and expenses had not been waived. View the most recent month-end performance and Top Ten Holdings for the Matthews Emerging Markets Equity Fund.

Background

At Matthews, it’s in our DNA to be cognizant to new windows of growth and to act on them. Over the past two decades, we’ve witnessed economies around the world become more interconnected, in part due to advancements in technology, innovation, and reconfiguration of supply chains. Dynamic companies with sustainable business models in Latin America, the Middle East and eastern Europe were not only growing domestically but also increasingly trading materials, equipment and end-market products with countries in Asia.

“We determined we could draw on our decades of deep expertise navigating Asia’s complex, volatile and under-researched markets to expand and invest in global emerging markets.”

In 2020, we believed these developments created genuine opportunities for investors to capitalize on growth beyond Asia in areas such as e-commerce, digital banking, wind and solar technology, and the electric vehicle (EV) industry. We also saw non-Asia emerging markets benefiting from ongoing structural changes such as rising demand for health care and higher-value consumer discretionary products.

Moreover, we determined we could draw on our decades of deep expertise navigating Asia’s complex, volatile and under-researched markets to expand and invest in global emerging markets. And we saw the potential to benefit from the increasing interconnection of emerging markets, as successful Asian companies traded and expanded into other regions.

All-weather strategy

The Matthews Emerging Markets Equity Fund embraces both a country level and bottom-up stock selection approach. At the Fund’s inception, as countries entered lockdowns and central banks lowered interest rates to boost consumption, we focused on company fundamentals, on corporate governance, and on the sustainability of business models.

As the years progressed, country-specific issues came to the fore as the U.S. Federal Reserve ratcheted up interest rates to manage inflationary pressures, introducing headwinds for markets particularly in Latin America, and geopolitical tensions between the U.S. and China increased. Toward the end of the five-year period, President Trump’s expansive new tariff policies reinforced the need for our country-level approach to complement our bottom-up stock selection.

“In recent years, countries and their environments have become much more impactful to market sentiment versus the fundamentals of individual companies.”

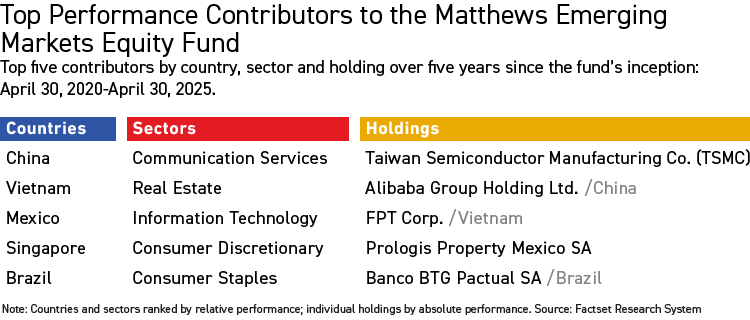

When we look back at the Fund’s performance contributors over five years, we can see how our multi-level strategy aided investment returns. China was the top contributor to relative performance, primarily because of our underweight position versus the benchmark. Stock selection in areas including communication services, information technology (IT) and consumer discretionary helped performance, while at the holdings level the top contributors were diversified across markets in Asia and Latin America.

Taking stock

I've been investing in emerging markets for over 30 years. The most common trait I have seen over the years is ‘change’ and in the last few years, countries and their environments have become much more impactful to market sentiment versus the fundamentals of individual companies.

Since the pandemic, for example, China’s markets have been impacted by geopolitics and domestic regulations, the United Arab Emirates (UAE) and Saudi Arabia, which were not even on the investment map a few years ago, are now generating increasingly interesting investment opportunities, while Latin America markets have shrunk but still offer avenues of growth. In India, we have seen exceptional economic growth that is now moderating with consumer spending softening, and Association of Southeast Asian Nations (ASEAN) markets have had mixed fortunes because of domestic political turmoil.

Emerging markets and Asia offer investors significant return potential but they are also areas that have significant volatility. While we are not short-term investors this doesn’t mean that we ‘buy and hold.’ We need to have a flexible approach and if we make mistakes it is important that we see them as early as possible and take action.

We think a country level and bottom-up stock selection approach is the best way to generate potential outperformance and manage risks in emerging markets. We assess the drivers of investment approach at the country level and at the company level—earnings growth, dividends, valuations and foreign exchange—which enables us to take offensive and defensive stances according to the potential opportunities and challenges that exist.

Within this framework we can also dig deep and identify thematic trends and idiosyncratic growth opportunities that may not exist for passive index investors.

The next five years

In our view, the beauty of emerging markets is quite simply their diversity. Some markets have little correlation to the global economy while others are more tied to international trade and trends. We believe the Matthews Emerging Markets Equity Fund is well positioned to potentially capitalize on these opportunities:

- Emerging markets are evolving and earnings are improving

- Economic growth and earnings growth are now taking hold in emerging markets and in developed markets in Asia post COVID, and consumption is rising.

- At the macro level, most emerging markets haven’t been burdened with high inflation, so we believe this will help them ease monetary policy if and when the Federal Reserve makes its next interest rate cut. We also expect a weakening U.S. dollar, which typically provides support for emerging markets.

- At the micro level, analyst consensus projects annualized total returns—including earnings growth, valuations and dividends—in emerging markets to be about 15% over the next 12 months, compared with approximately 9% for the U.S., and developed markets in Europe, Australasia and the Far East.1

- Governance impact on earnings growth

- In our view, better governance can significantly improve earnings growth and in emerging markets stewardship is improving as the structure of companies, their transparency and their accountability, is getting better. Additionally, access to management is helping investors like Matthews engage with companies and improve corporate governance.

- In specific markets like South Korea, reforms related to capital efficiencies are triggering an increase in stock buybacks and dividends by companies as they seek to increase their valuations and release excess cash on their balance sheets.

- Avoiding correlation with the U.S.

- We are mindful of markets with deep correlations to the U.S., in terms of trade or supply chains. We focus on opportunities driven by domestic demand. The prime examples of such markets are India and China where most activity is geared to serving the internal economy. In India, domestic growth areas include financials and manufacturing, and in China, growth has been robust in e-commerce, EVs and internet platforms.

- We also recognize growth opportunities in traditional emerging markets, such as Turkey and Greece, and in Latin America, which are still expanding through urbanization and wealth generation and are supported by macro tailwinds like lower interest rates and a weaker dollar.

- The developed parts of emerging markets, like South Korea and Taiwan, are benefiting from the global artificial intelligence (AI) boom and their foundry industries dominate the chipmaking supply chain. But these markets are dependent on U.S. big tech firms maintaining their billion-dollar CapEx plans and this is not a given if a slowdown in the U.S. becomes evident.

- China

- An eventual recovery in China’s real estate sector will be a tailwind for the broader economy and consumer confidence but we believe there are positive signs in China’s markets today.

- Earnings growth in Hong Kong-listed stocks is improving and valuations remain compelling.

- We also believe the innovations in China’s economy go well beyond AI and are helping to drive biotech, robotics and EVs.

- Not just Asia

- The Middle East is a troubled region but we believe markets like the UAE and Saudi Arabia can’t be ignored. The economies of these markets are developing beyond oil and are increasingly embedding with economies and companies in Asia.

- In Latin America, valuations are generally compelling, with significant upside potential in our view, mainly tied to a declining interest rate environment. Rates in Mexico and Brazil could take a downward trajectory and support the manufacturing and commodity-driven economies of these countries.

1 Source: Bloomberg; Matthews - May, 2025. The economic and market forecasts presented herein have been generated as of 05/20/2025 and provided for informational purposes only. Forecasts are based on third-party sources or information and there can be no assurance or guarantee that the forecasts can or will be achieved.

As of 12/31/25, the average annual total returns for the Matthews Emerging Markets Equity Fund – Investor Class for the one-year, three-year, five and since inception (4/30/2020) periods were 29.39%, 15.95%, 4.15% and 12.75%, respectively. That compares with the MSCI Emerging Markets Index which gained 34.36%, 16.98%, 4.67% and 10.78%, respectively. As of 12/31/25, the one-, five-, and 10-year returns for the MSCI AC Asia ex Japan Index were 33.02%, 4.16% and 8.92%, respectively, and for the MSCI AC Asia Pacific Index were 28.59%, 5.36% and 8.45%, respectively.

Matthews Emerging Markets Fund Fund–Investor Class Gross Expense Ratio 2.45%, Net Expense Ratio 1.11%. Matthews has contractually agreed to waive fees and reimburse expenses to limit the Total Annual Fund Operating Expenses until April 30, 2026. Please see the Fund’s prospectus for additional details.