Looking Up for EM

Vivek Tanneeru, portfolio manager, sees structural and cyclical tailwinds converging for emerging markets equities.

SubscribeIt’s tempting to take the underperformance of emerging markets in relation to developed markets over the past decade and use it as a yardstick to judge future growth. In our view, that would not only overlook the strong potential of emerging markets for growth and portfolio diversification but fail to grasp the long-term drivers that worked to shape these markets in the past and that will likely work to shape them again.

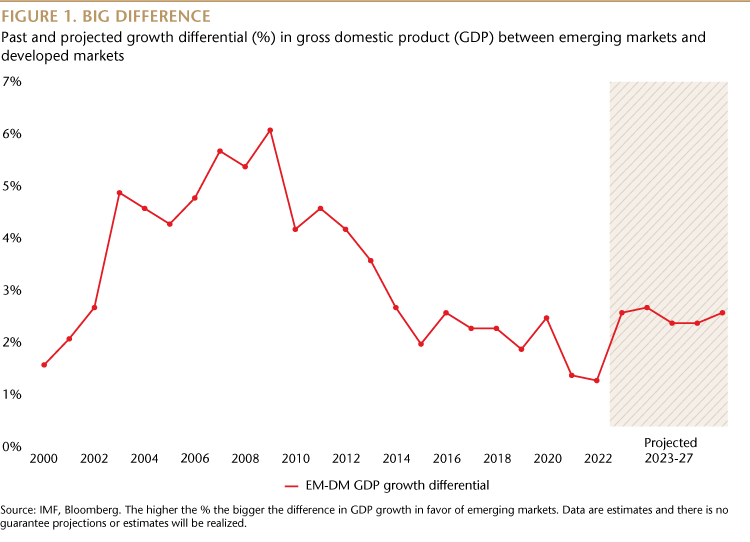

It's no secret that emerging markets underperformed U.S. equities over the last 10 years or so. But in the prior decade the opposite was true. So what were some of the underlying forces that made these two things happen? Well, one of them was a change in the so-called growth differential in gross domestic product (GDP) between emerging markets and developed markets. At the turn of the century, the differential began to expand in favor of emerging markets. Equities in emerging markets then went on to outperform developed market equities, including U.S. stocks, significantly in the 2000s. By the 2010s that trend started to reverse. As the economic growth differential narrowed so western stocks started to outperform emerging markets stocks. This year, the growth differential sits at the lowest point since 1999, in the immediate aftermath of the Asian Financial Crisis.

There are of course many drivers of equity market performance besides GDP growth, including money supply, valuations, market composition, geo-political and regulatory developments and governance standards. But economic expansion and earnings growth are a key buoyancy aid for markets. While strong GDP performance doesn’t always result in strong equity performance, especially in the short-term, it does generally lead to faster corporate topline growth. Under the right conditions, such as when capacity utilization rates increase, topline growth can lead to attractive earnings growth and this in turn over the long-term can provide upside pressure for stock prices. Higher earnings growth can then lead to higher returns on equity and ultimately higher price-to-book ratios.

“It’s reasonable to consider the possibility that emerging markets’ earnings growth may pick up and valuation discounts will narrow, potentially leading to improved relative performance.”

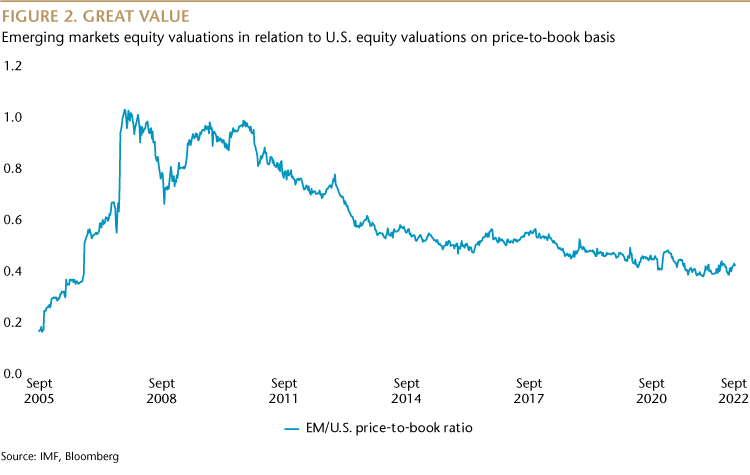

As well as this structural correlation between equity performance and GDP growth there is a cyclical correlation between relative valuation and GDP growth. During the 2000s, emerging markets equities narrowed the valuation discount on a price-to-book basis in relation to U.S. stocks as the GDP growth differential widened, earnings growth picked up and return metrics improved. Valuations achieved parity with U.S. markets and at the end of the decade emerging markets equities had outperformed U.S. equities by 286%. In the 2010s, as the GDP growth differential narrowed, the valuation discount expanded and U.S. equities have outperformed emerging markets by 262% over the past 12 years.

Return to growth

In light of these past long-term correlations we may wonder how the GDP growth differential between emerging markets and developed markets will behave in the future. Will it narrow or will it widen? In the medium term, there is some visibility. The International Monetary Fund (IMF) projects that between 2023 and 2027, the growth differential will widen again and return to the levels seen in mid 2010s. It’s perhaps reasonable therefore to consider the possibility that emerging markets’ earnings growth may pick up and valuation discounts will narrow, potentially leading to improved relative performance compared with the U.S. equities.

In addition to the beneficial structural impact on emerging markets of stronger GDP growth relative to developed markets, other cyclical factors may also be at play. For example, major emerging markets are less likely to be adversely impacted by rising U.S. interest rates and a strong U.S. dollar. This is for two reasons. Firstly, inflation isn’t a big problem in many emerging markets, such as Saudi Arabia and China, where it is running at around 3% and below.

Secondly, in emerging markets where there has been higher inflation, the central banks of these nations started raising rates very early to clamp down on rising prices. Brazil, for example, started hiking rates in March 2021. Mexico also did a good job of raising rates early. It’s not a surprise that both of those currencies have appreciated against the U.S. dollar. The currencies of major emerging markets in many cases have stood up to the dollar better than some developed market currencies, such as the euro, the Japanese yen and the British pound. That’s no mean feat and different from the past cycles.

Emerging markets also have growth engines that are either the equivalent to or on a bigger scale to what developed markets have to offer. Investment in innovation among the biggest five emerging markets, for example, is comparable to that of the top five developed markets. In terms of sustainable investing, emerging markets companies are at the forefront of addressing the world's most pressing challenges, such as climate change, access to affordable healthcare and housing and financial inclusion, in an innovative and profitable fashion and at scale. Both of these themes will be a boon when the economic growth differential starts to expand in emerging markets’ favor.

In conclusion, we believe the past can inform the future provided we look far enough back and grasp what the cyclical drivers behind long-term changes have been. Economic projections suggest the tide is turning and in our view emerging markets are structurally and cyclically nicely poised for the medium-to-long term.

Vivek Tanneeru

Portfolio Manager

Matthews Asia

Definition:

Capacity utilization rate: measures the percentage of an entity’s potential output that is actually being realized.