Three Things Needed to Nurture Innovation

Portfolio Manager Michael Oh, CFA, uncovers three things needed for innovation in companies.

Where are we in the innovation-driven growth cycle in Asia? I believe that we are standing in the very early innings of this innovation-driven growth era and here's why. For innovation to take place, you need three things. First, you need very strong human resources. Second, you must have vibrant capital markets to support these companies. And third, you must have a very large addressable market. Now with rising income levels, Asia has all three.

1. Strong Human Resources

Asia has one of the largest, highly educated, well-trained workforce today. Asia produces more PhDs than Europe or the US, and that's not including Asian students studying abroad who may return to their native countries.

2. Vibrant Capital Markets

The second piece is vibrant capital markets, active venture capital and equity markets to support these companies. Today, Asia is one of the biggest markets for venture capitalists and equity markets.

3. Large Addressable Markets

You need a large addressable market, otherwise you cannot expect innovations to create much value. And today, Asia has the world's largest consumer market, bigger than the US and Europe.

History Repeats Itself?

The last time we saw this was in the U.S. in the '70s. Think about what happened then, the U.S. passed around $8,000 income level back in the '70s. Around that time we had a ‘big bang’ of innovative companies like Microsoft, Nike, and Genentech, and they're still leading innovation today. All of these companies were born to serve the needs of the US market first, and then they grew to be global giants and created tremendous value for investors. For example, Microsoft and Nike have returned approximately 20% per annum since their public listings.1 Also, innovative industries in consumer, healthcare, and technology sectors clearly outperformed the broader S&P 500, and these are the sectors that Matthews’ innovator strategies are focusing on. We believe Asia now is where the U.S. was back in the '70s, and we are beginning to see an emergence of many innovative companies.

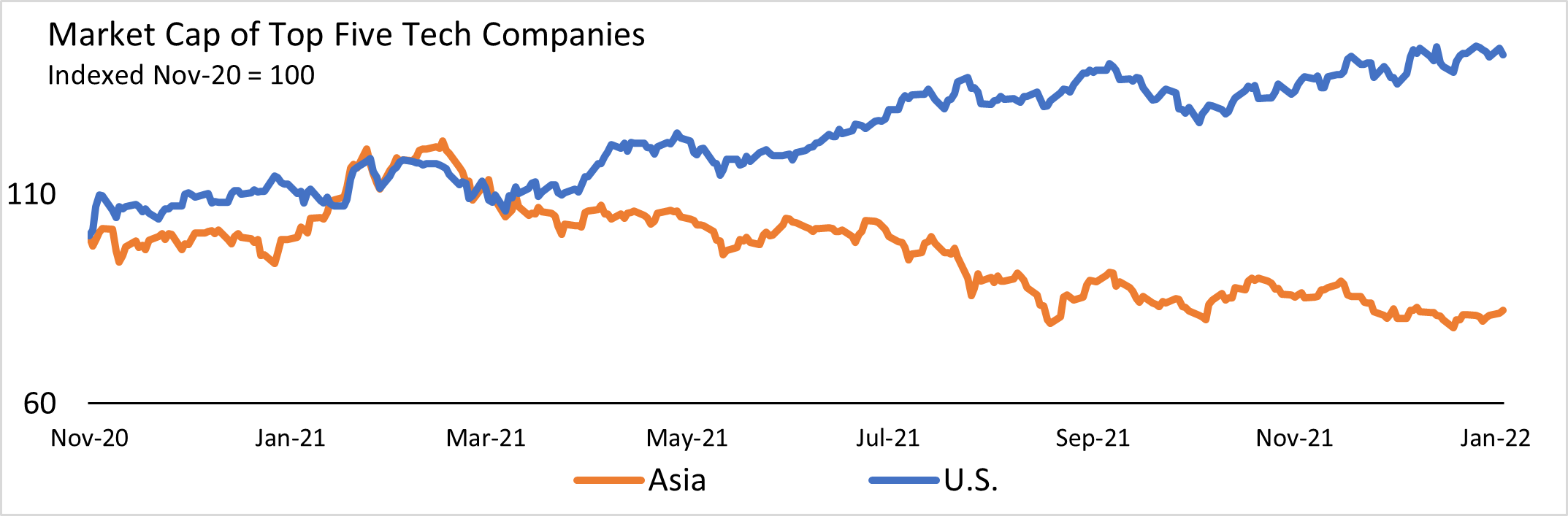

Since regulatory reform began in November 2020, there has been a very clear divergence between the U.S. and China, as you can see in Chart 1. A few things that I've learned about companies in China; they don't have to reinvent their business model because of these reforms, they just need to adjust their strategy to make sure they're complying with a new regulatory environment. Companies like Tencent may continue to be competitive globally and Alibaba may continue to be an e-commerce giant in China. I believe that the aim of the Chinese government is trying to protect consumers’ rights and they're not trying to break up these companies.

Chart 1. Asia ex Japan vs. U.S.

Source: FactSet Research Systems; data as of January 4, 2022

There is no guarantee any estimates or projections will be realized.

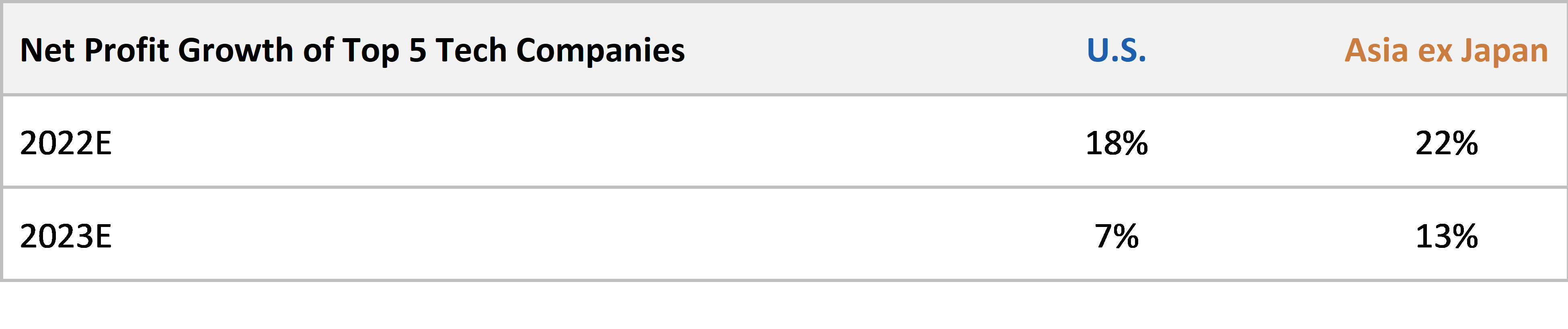

If you look at the top five biggest technology companies in Asia ex-Japan versus the U.S., you see a clear divergence between the two. This tells me that selloff in Asia was mostly driven by sentiment rather than the fundamentals of these companies.

These are some of the opportunities that we see on the ground. If you look at the new economy areas, electric vehicles (EVs) or green energy space, Asia is leading many innovations today. 90% of all EV cars produced have batteries made by Asian companies or companies in partnership with Asian companies. Some of the biggest markets for new green energy are now in Asia, and some of the biggest producers of green energy-related products are also by Asian companies. One of the big themes we see across the globe is automation. And if you look at who's leading automation today, it’s mostly led by companies in Korea, Japan, and increasingly more out of companies in China as well. All these things sum up why we focus on innovative companies in Asia today and why we believe that focusing on innovation is one of the best ways to approach when you're looking for growth companies in Asia.

Michael J. Oh, CFA

Portfolio Manager

Matthews Asia

As of 12/14/2022, accounts managed by Matthews Asia portfolios held positions in Tencent and Alibaba. As of 12/14/2022, accounts managed by Matthews Asia did not hold positions in Microsoft, Nike or Genentech.

1As of 12/14/2022, Microsoft has returned 25.4% annualized since their IPO, Nike has returned 18.2% since their IPO. Source: FactSet