Spotlight on the Matthews Emerging Markets ex China Active ETF

Emerging markets can offer investors the biggest potential for long-term growth over most other equity assets classes, in our view. The Matthews Emerging Markets ex China Active ETF (MEMX) provides investors exposure to the growing abundance of quality companies that emerging markets may have to offer while giving them more control over their holdings in China.

What is the objective of the Matthews Emerging Markets ex China Active ETF (MEMX)?

The investment objective of the Matthews Emerging Markets ex China Active ETF (MEMX) is to achieve long-term capital appreciation. MEMX seeks to achieve its objective by investing at least 80% of its net assets in companies located in emerging markets excluding China. MEMX takes an all-cap approach and focuses on companies that are capable of sustainable growth based on their fundamental characteristics.

Emerging market countries generally include every country in the world except the U.S., Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging market countries with newer or even less developed economies and markets, such as Sri Lanka and Vietnam.

Why are you launching an ETF that invests in emerging markets excluding China?

Many investors want broad exposure to emerging markets without China. There are two principal reasons. Some investors are uncomfortable with China and don’t want to make direct investments there. However, these investors still recognize the need to gain exposure to the rest of emerging markets which is deep, diverse and contains most of the world’s population within its purview. Conversely, other investors see China as meriting its own single country allocation due to the country’s size and market depth. These investors can use an emerging markets ex-China ETF in conjunction with a dedicated China allocation to gain broad exposure of emerging markets and with no unintended overlap. An emerging markets ex-China ETF allows investors to customize and decide how much China they want by making it a separate allocation decision.

"In a nutshell, MEMX enables investors to take control of their China exposure."

We believe MEMX services these needs and enables investors to get greater exposure to emerging markets beyond China. It provides for greater diversification and less single-country risk and the potential for alpha contribution from smaller emerging markets. In a nutshell, MEMX enables investors to take control of their China exposure. For some investors, MEMX can serve as a completion strategy to a core, dedicated China allocation like the Matthews China Active ETF (MCH), and for other investors MEMX may be a way to avoid investing in China or reducing exposure to China while still investing in a potential high-growth asset class.

Is the Matthews Emerging Markets ex China Active ETF (MEMX) the same as the Matthews Emerging Markets Equity Active ETF (MEM) strategy but without exposure to China?

We view the Matthews Emerging Markets ex China Active ETF (MEMX) as a subset or an extension of the Matthews Emerging Markets Equity Active ETF (MEM). We've kept the approach simple. Aside from excluding China, the investment approach is the same as the MEM. MEMX employs a bottom-up stock-picking strategy focused on companies rather than themes and geographical markets. It takes advantage of Matthews’ deep experience and understanding of emerging markets and will be managed by investment managers with a track record of identifying long-term growth opportunities in the asset class.

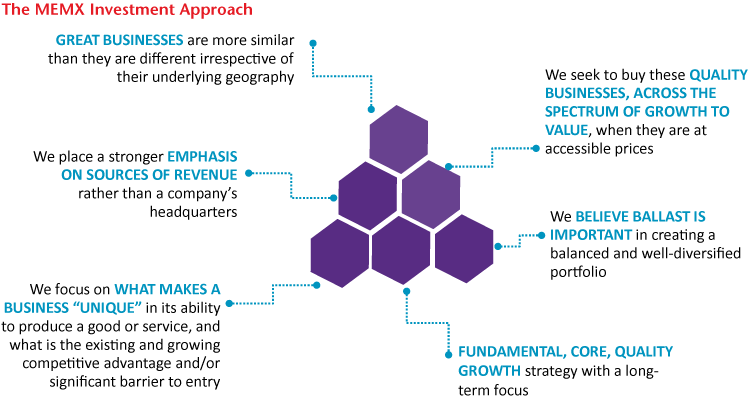

Describe in more detail the investment approach?

MEMX takes a company-first investment approach that emphasizes fundamental analysis over top-down country or sector allocation. The investment process centers on the fundamental analysis of a company, an assessment of the industry and competitive landscape and a determination of the valuation of the business.

We focus on where and how a company makes money. We seek out high-growth, high-quality companies across emerging markets and across the market capitalization spectrum. We regard trends as tailwinds rather than drivers of our investment decisions. As bottom-up portfolio managers, we also see ourselves as partial owners of the businesses in which we invest. And by employing an all-cap approach, we believe small companies may offer attractive potential for generating alpha and that incumbency can be an advantage that compounds over time. With this approach, we are guided by a six-point philosophy:

How do you assess the strength of a business?

Companies are evaluated holistically. We are ultimately trying to answer some very basic questions:

- Do I want to be an owner of this business?

- Is the management team working for me, as a minority shareholder?

- Is the price on offer appropriate for a long-term holder?

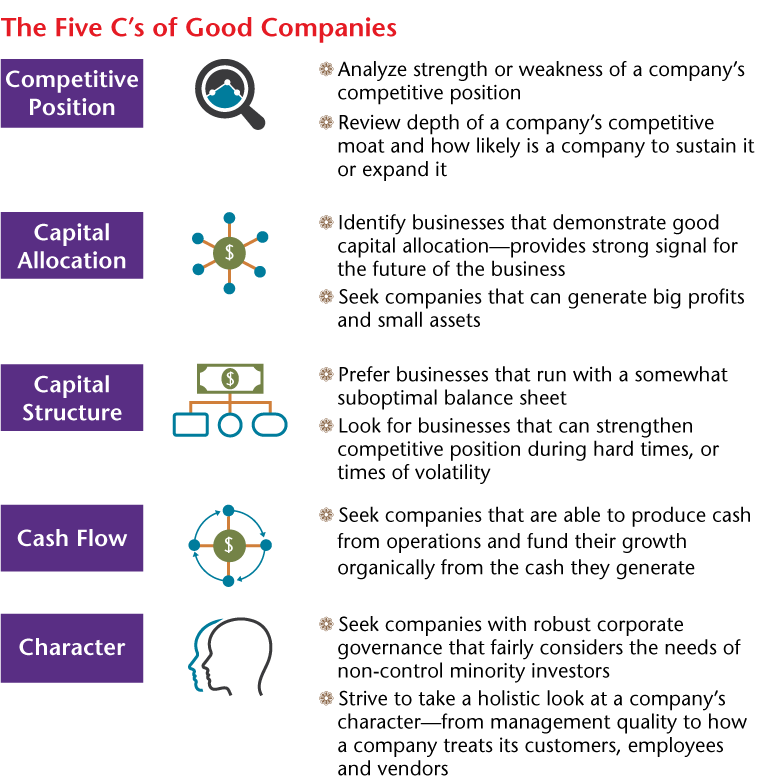

Answering these questions requires assessment of “the Five Cs” framework which homes in on a company’s competitive position, its process for capital allocation, its capital structure, its cash generation potential and its character. Holistic analysis requires understanding the drivers captured inside and outside financial statements. Financial metrics may include evaluation of margins, cash flow conversion and debt metrics. Attributes important to the investment decision that aren’t included in financial statements might include brand resonance with consumers, relationship with regulators, character of management, company culture, or other such variables. In our experience, the characteristics of a good quality company are consistent across the investment universe irrespective of the market they are in or sector they operate in.

How do you construct your portfolio?

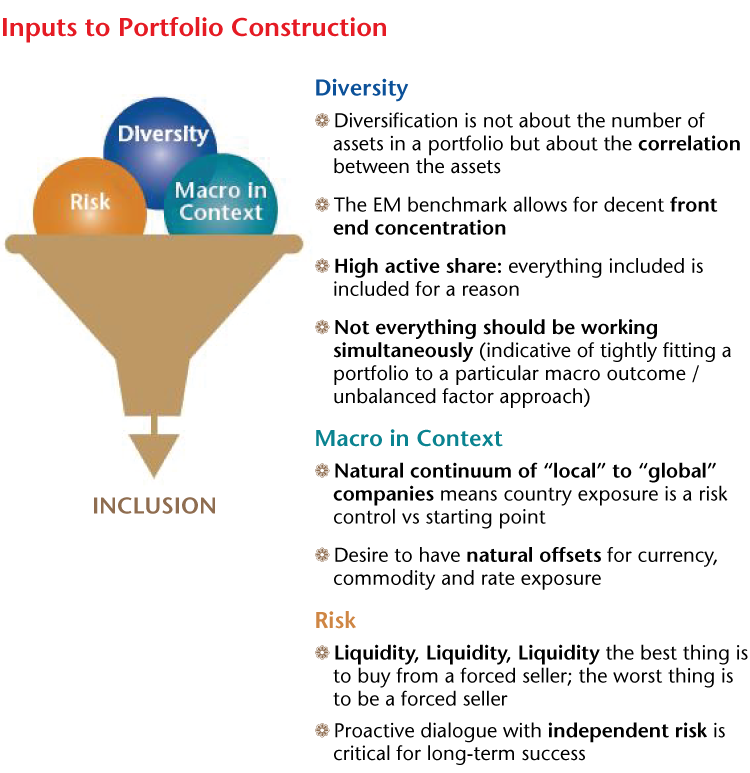

Portfolio construction for MEMX balances conviction and humility. A well-constructed portfolio is not a list of “best ideas.” It should contain “ballast” holdings that allows the strategy to help weather an unwritten future.

New positions will tend to be modestly sized, in the range of approximately 0.5% to 1% of the total portfolio, and the largest positions will tend not to exceed 5% to 6%. The team will use a milestone-based approach to increasing conviction and position weight. These milestones are typically nonfinancial and focus on the execution of stages of the long-term growth strategy by the company. Over time, the team is able to assess the “intentionality” of management—for example, did they do what they previously said they would do? Measuring intentionality takes time. As the team’s understanding and conviction in a company increases, then sizing may also increase.

MEMX has a long-term investment horizon and seeks to hold positions for as long as possible. This should result in low turnover over time, but we do not numerically target this. Periods of higher volatility (such as in recent years) may result in turnover that is higher than those with low volatility.

How do you determine country weights in the portfolio?

We focus on companies as our starting point, rather than countries. We believe the best chances of capturing durable growth come from strategies that prioritize company selection over country allocation. Country weights are heavily influenced by the business model of where a company falls on the continuum of local to global competition. A semiconductor company may have little to do with its assigned geography whereas a food retailer is entirely driven by it. Over the course of a market cycle, the portfolio’s exposure to any individual country may fluctuate. With an unconstrained and benchmark agnostic approach in terms of country, sector and company allocations, exposures are a by-product of bottom-up security selection.

Do you undertake on-the-ground research?

Given the long-term holding periods, company visits and meetings are an essential part of the investment process. They give us better insight into a company’s business model and growth prospects as well as management’s thoughts on business strategy and capital allocation. The meetings also provide a good opportunity for us to gain a greater understanding of the management team and their intentions for the company. These on-the-ground meetings are important as companies in emerging and frontier markets are substantially smaller, less liquid and more volatile than securities markets in more developed markets.

A first meeting with a new company will provide an opportunity to firstly, understand the firm’s management strategy, track record and long-term business prospects, and secondly, assess the company’s governance standards. It is vital the team develops a positive view of the governance practices before investing in a company. We believe that by investing in quality companies we have the potential to yield impressive returns with a lower risk of permanent loss of capital. Once the company is in the portfolio, we continue to maintain regular meetings to ensure that we continue to have confidence in both the business and its management.

Why does corporate governance play an important role in your investment process?

Matthews Asia has, since its inception in 1991, always placed a significant emphasis on corporate governance in making investment decisions. The fair treatment of minority shareholders is an important consideration for us. Across all our strategies, Matthews Asia has always made a commitment to invest in companies that demonstrate sound corporate governance. Our belief is that an investor’s best interests are served through companies that exercise responsible ownership and that this can improve shareholder returns over the long term.

How does the ETF undertake risk management?

The largest variable any investor must address is the future, which by definition is unwritten and uncertain. Humility is important and must balance out conviction. Risk and reward are two sides to the same coin. Risk features prominently in the security selection and construction process. This focus at the portfolio level includes thinking through the correlations between underlying positions and ensuring adequate diversity within MEMX.

Matthews Asia has developed a rigorous and tested approach to risk management with three levels:

- Portfolio Level—through the in-depth company due diligence process performed by our Investment professionals and their continuing focus on avoiding permanent impairment of capital

- Matthews Asia CIO Level—through oversight and review of the portfolio to help ensure consistency with the investment goals and objectives and a review of portfolio risk and liquidity

- Matthews Asia Enterprise Level—through independent risk and compliance monitoring performed by our Control Side functions (Legal, Investment Risk, Compliance, Operations/IT, Fund Admin and Finance) and our Governance process which was designed to ensure that all significant risks are escalated to and discussed with senior management.

What experience does the portfolio management team have?

The MEMX portfolio team has significant experience investing in emerging markets, including the Asia region. Prior to joining the firm in 2018, Lead Manager John Paul Lech spent nearly 10 years at OppenheimerFunds as an analyst and portfolio manager on a global emerging markets equity strategy. John Paul was the first analyst hired by Oppenheimer in 2008 for the strategy, conducting primary research on companies across Asia, including China and India, and other emerging markets like Brazil, Russia and Mexico. He has experience analyzing and formulating investment theses in a variety of sectors.

Prior to joining the firm in 2020, Co-Manager Alex Zarechnak spent a total of 15 years (1998 – 2006 and 2012 – 2019) at Wellington Management as an analyst for the firm’s flagship Emerging Markets Equity fund—as a generalist first covering Central and Eastern Europe, the Middle East and Africa (CEEMEA), then Latin America. From 2006-2012, he was a regional equity analyst at Capital Group, covering emerging markets with a focus on energy, telecoms and consumer sectors in Latin America and CEEMEA. Alex began his emerging markets career as a Russia equity analyst with Templeton Emerging Markets, based in Moscow.